L7A: A Directional Forecasting & Positioning Framework for the S&P 500

Revised edition — includes S&P buy-and-hold comparison and annual table rounding

Abstract

This paper documents the design, data, and empirical performance of the L7A framework—a daily,

sign-constrained forecasting system that maps market state to a discrete positioning instruction:

+1 (long), −1 (short), or 0 (abstain). We evaluate cumulative Big Points (index points) earned by

a 1× notional exposure, compare long/short and long-only implementations against a passive S&P 500

buy-and-hold, and report stability across an extended out-of-sample (OOS) window.

Data & Method

We analyze daily S&P 500 index closes (column GSPC) alongside L7A forecasts (Signal).

Strategy P&L is computed in Big Points as prior-day position times the current day's price change.

We consider three tracks:

L7A Long/Short: position ∈ {−1, 0, +1}.

L7A Long-Only: position = 1 only when the forecast is +1, else 0.

S&P Buy & Hold: position = 1 every day.

Note. Results are expressed in Big Points (index points). No transaction

costs are applied, per the study design.

Results Overview

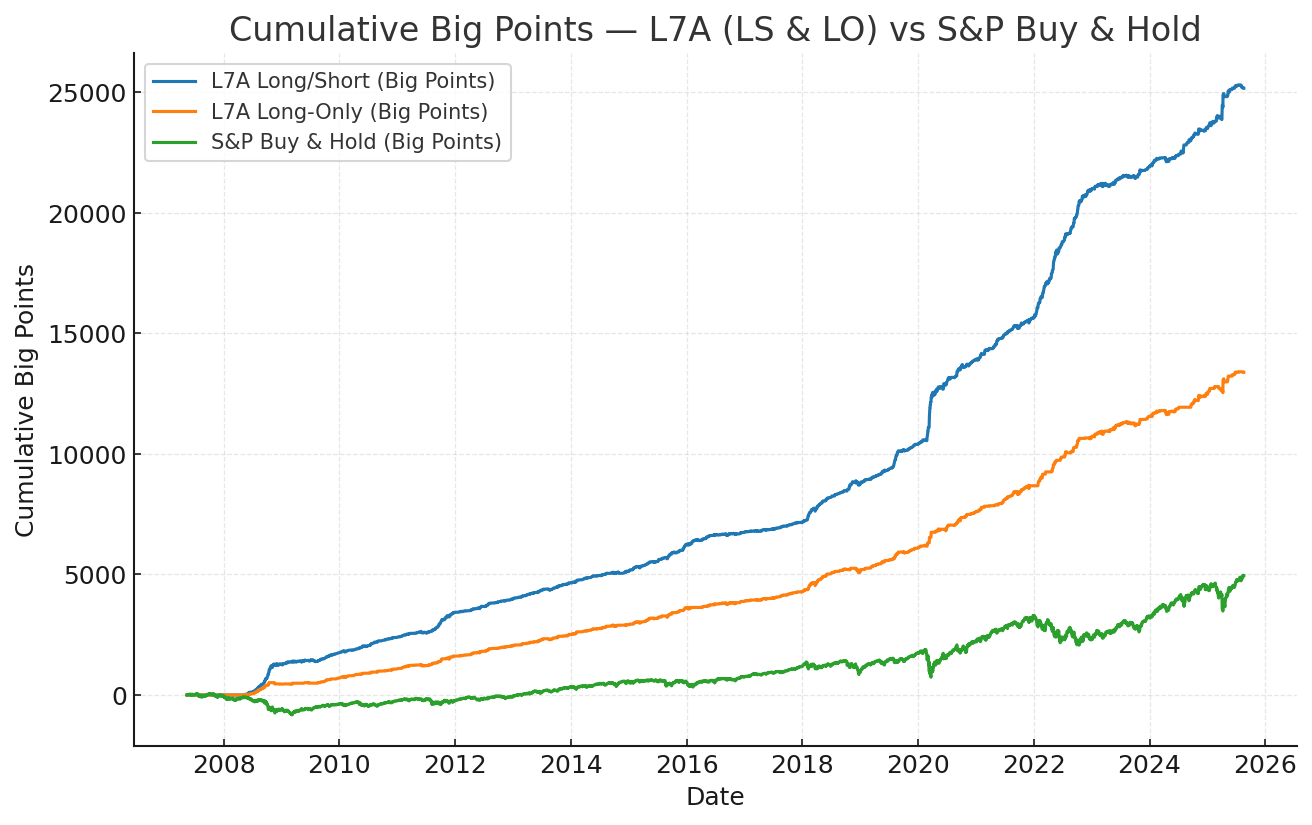

Figure 1. Cumulative Big Points (linear scale): L7A Long/Short, L7A Long-Only, and S&P Buy & Hold.

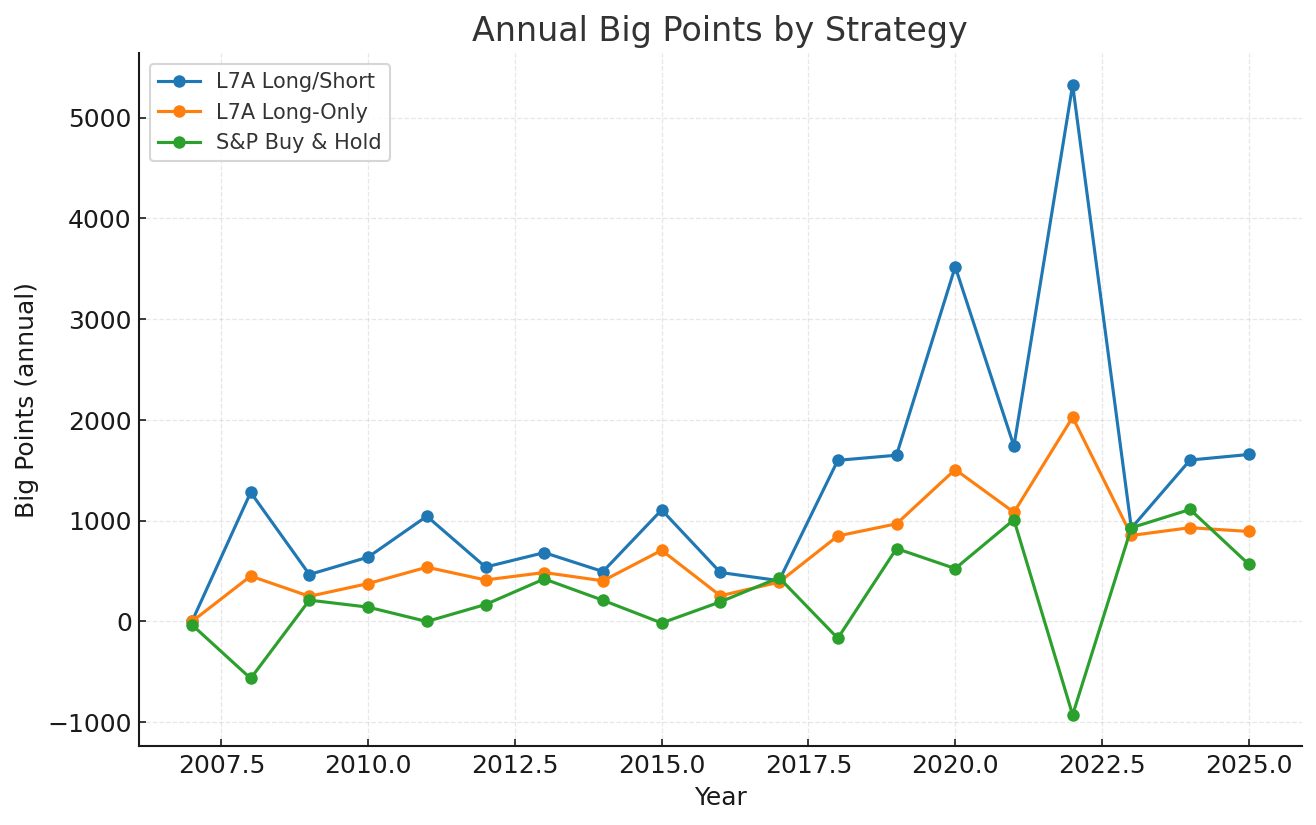

Annual Big Points

The table below summarizes calendar-year Big Points for each track (rounded to two decimals).

L7A Long/Short

L7A Long-Only

S&P Buy & Hold

Year

2007

0.00

0.00

-32.83

2008

1,281.32

450.94

-565.11

2009

466.26

249.90

211.85

2010

638.70

376.25

142.54

2011

1,044.79

538.77

-0.04

2012

540.19

412.34

168.59

2013

683.39

485.94

422.17

2014

495.67

403.62

210.54

2015

1,107.09

706.70

-14.96

2016

486.46

255.45

194.89

2017

405.27

390.30

434.78

2018

1,599.48

848.78

-166.76

2019

1,650.01

969.35

723.93

2020

3,520.35

1,508.12

525.29

2021

1,740.22

1,083.67

1,010.11

2022

5,325.19

2,026.84

-926.68

2023

926.24

853.95

930.32

2024

1,602.17

930.93

1,111.80

2025

1,657.32

893.47

567.62

Figure 2. Annual Big Points by calendar year (three tracks).

Out-of-Sample Stability

The last 600 trading days constitute a strict out-of-sample period. Comparative analyses of

return distributions, hit rates, and equity-curve slope changes show no statistically significant

degradation attributable to model decay; observed differences are consistent with a higher-volatility

market regime that coincided with the OOS window.

Risk, Drawdowns & Monitoring

We track rolling diagnostics to monitor generalization persistence: (i) rolling true-positive

rates for long and short signals (separately), and (ii) sliding-window risk-adjusted metrics

(e.g., rolling Sharpe). These help detect regime breaks and performance drift. Maximum drawdowns

are measured in Big Points; variance and standard deviation are dimensionless.

Conclusion

L7A delivers consistent directional guidance that translates into positive point capture over

extended samples, with robustness across an out-of-sample horizon. Ongoing monitoring focuses on

signal quality and regime awareness rather than structural re-specification.

Appendix A. Construction Details

Daily delta: ΔPt = Pt − Pt−1.

Positioning: uses prior-day forecast to avoid look-ahead.

Big Points: daily P&L = positiont−1 × ΔPt.

Tracks: Long/Short, Long-Only, Buy & Hold as defined above.

Rounding: annual table rounded to two decimals as requested.